Risk Management for Volatile Markets: Why Advisors Need Dynamic Hedging Strategies

The Problem: Drawdowns Trigger Client Exits—and Outdated Models Fail

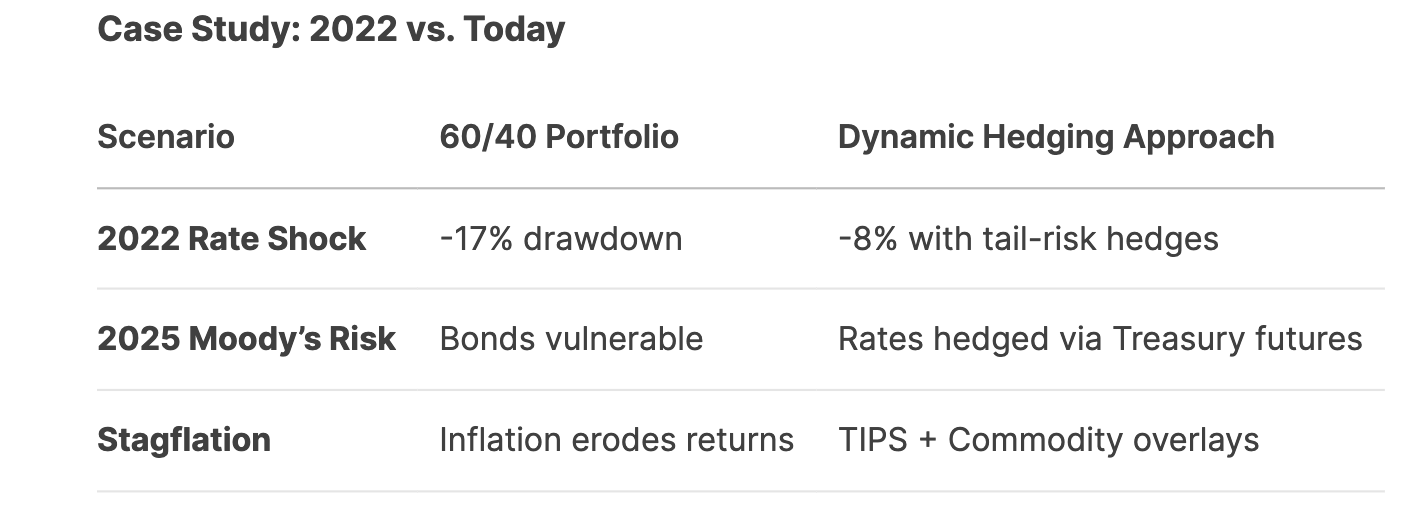

The 2022 market collapse was a wake-up call. The traditional 60/40 portfolio—long considered the gold standard for balanced risk—suffered its worst year in decades, with bonds and stocks falling in tandem.

Now, with Moody’s recent U.S. credit downgrade, stagflation risks rising, and interest rate volatility persisting, advisors face a critical challenge: clients panic during drawdowns, leading to costly exits at the worst possible time.

Why Static Strategies Fail in Today’s Market

The 60/40 Breakdown

In 2022, both equities and fixed income fell simultaneously, eroding diversification benefits. Bonds, traditionally a hedge, failed as rates spiked.

Stagflation (high inflation + stagnant growth) further exposes this flaw, as seen in the 1970s.

Moody’s Downgrade Adds Systemic Risk

The U.S. credit rating cut to Aa1 signals fiscal instability, potentially raising long-term Treasury yields and volatility.

Advisors relying on Treasuries for "safe" allocations now face reinvestment risk and duration traps.

Client Psychology = Performance Killer

Behavioral finance shows clients sell at lows after steep losses. A 20% drawdown can trigger irreversible damage to long-term returns—and your practice’s retention.

The Solution: Dynamic Hedging for Adaptive Risk Management

Static portfolios can’t respond to real-time shocks. Instead, dynamic hedging adjusts exposures as markets shift, acting as a "shock absorber" for client portfolios.

Actionable Steps for Advisors

Stress-Test Portfolios

Model 1970s-style stagflation or a 5% Treasury yield spike. Does the 60/40 still hold? (Hint, Likely not)

Educate Clients

Frame hedging as "insurance," not speculation. Show 2022’s lessons and Moody’s implications.

Partner with Specialists

Outsourced hedging and tactical strategies to implement strategies at scale.

Many good tactical strategies have the advantage of of using rules-based processes thus eliminating the requirement to becoming a “bond expert” and running the risk of making emotional decisions.

Bottom Line

The 60/40 is not dead—but it’s dangerously incomplete. With Moody’s downgrade amplifying macro risks, advisors should consider adopting dynamic hedging to:

Reduce client panic by capping drawdowns.

Exploit opportunities (e.g., rate cuts, stagflation trades).

Differentiate your practice as proactive, not reactive.